Topic 10:

CONTROLLING

Chapter 20 in Text Book

Pages: 556 - 581

Key topics in this chapter :

Ñ What is Controlling

Ñ Why is Control Needed ?

Ñ The Control Process

Ñ Techniques of Managerial Control

Ñ Budgetary Control

Ñ Types of Business Budgets

Ñ Uses of Budgets and Budgetary Control

Ñ Features of a Good Control System

What is Controlling

In controlling , managers evaluate how well the organization is achieving it's goals and takes corrective action to improve performance. Managers monitor individuals, departments, and the organization to determine if desired performance has been reached. Managers also take corrective action to increase performance as required. The outcome of the controlling function is accurate measurement of performance and regulation of efficiency and effectiveness. Thus controlling may be defined as the process of ensuring that the actual activities conform to the planned activities.

Why is Control Needed ?

· To create better quality of people, products and processes

· To cope with changes, both internal and external

· To create faster cycles of production, leading to greater efficiency and effectiveness.

· To facilitate delegation and teamwork

· To add value

Example: General Electric found that leaders must make extra efforts to push new quality programs. They tell employees that quality is critical to survival, you have to demand everybody gets trained, you have to cheerlead, you have to have incentive systems, you have to say 'We must do this'.

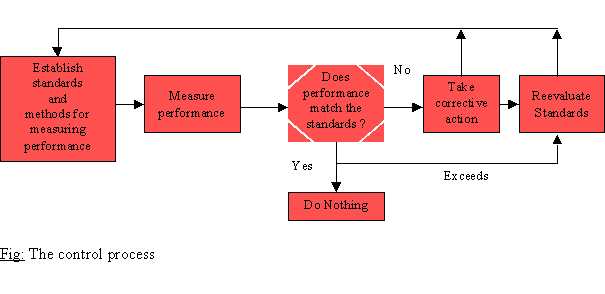

The Control Process

The first step in the control process is the setting up of standards of performance. The standards should be set in measurable terms such as in terms of physical units produced, costs, profit, time etc.

The second step requires the measurement of the work actually done and the result achieved. Measurement of performance should be done in the same units as the set standards to make the comparison easier. However, measurement of performance at the higher levels of management becomes difficult as the results achieved cannot be so easily apportioned to the

different tasks. Measurement of the actual performance may be at periodic intervals - weekly, monthly, quarterly or yearly.

After measuring the performance we have to find out if there are any deviations, and moreover we also need to find out what the causes of these deviations are. These can be found out through a detailed analysis.

The purpose of controlling is not merely to find out the causes of the deviations but also to adopt various remedial measures. Where the deviations cannot be rectified through managerial actions, the standards set may have to be revised to make them more realistic.

It should also be remembered that controlling should take place at all stages of the work process. Thus control can be more effective and timely when it is use before the process, during the process and after the work process. Moreover, controlling is not merely a function covering the blue collar workers, it is applicable even to review the performances of the management and at all types of organisations.

Example: Continuous improvement is the theme of the US Army's After Action Review program. Exercises are videotaped and monitored by trained observer controllers. The results are peer reviewed, with participants commenting on one another's performances and the observer-controllers giving immediate feedback.

Techniques of Managerial Control

Various techniques are used by management to control the diverse activities of the organization. Some of these techniques include:

· Statistical control reports : using averages, correlation etc. for example average daily/monthly sales, employee turnover etc.

· Break even point analysis : to anticipate the profit (loss) at various levels of production and sales.

· Special control reports to monitor the performance in a particular area like handling of customer complaints.

· Gantt milestone chart to check the production schedule at different levels.

· Programme Evaluation and Review Technique (PERT)

· Critical Path Method

· Cost Control

· Management Accounting

· Production Control

· Quality Control

· Budgetary Control

Budgetary Control

Managerial decisions frequently have implications for a number of functions of a business. It is very important for managers to co-ordinate these interrelated aspects of decision making. One way for managers to co-ordinate their activities is to prepare detailed and explicit plans

of action for specific future periods. These plans are referred to as Budgets and the co-ordinating activity is usually termed as Budgetary Control. Thus budgets may be defined as a formal quantitative statement of resources allocated for planned activities over stipulated periods of time.

A budget is prepared for a definite future period which is defined well in advance. The period selected may be short or long range depending on various factors such as the life cycle of the firm’s products, the type of customers, the stability of demand for the firm’s products,

In many organisations budget help frame an entire programme covering all operations of the enterprise. Many individual budgets are developed in different departments and subsequently integrated into one master budget. As the size of the organisation increases, the need for budget also becomes more.

Types of Business Budgets

Within the purview and framework of the master budget or the general budget of the firm, a number of sub-budgets for different business operations are prepared. Functional budgets may include the following:

· Sales Budget including Selling and Distribution Cost Budget

· Production Budget which consists of :

Raw Materials Budget

Labour Budget

Manufacturing Overhead Budget

· Personnel Budget

· Plant Utilization Budget

· Administration Cost Budget

· Capital Expenditure Budget

· Research and Development Cost Budget

· Cost Budget

Such functional budgets are first developed for integrating them into a master budget. The nature of the budgets depend primarily on the nature of the activities of the enterprise and the purposes which the budgets are intended to serve. While some organisations follow the Incremental Budgeting approach, others follow the Zero Based Budget approach. Both these approaches have their advantages and disadvantages and therefore some organisations adopt the Priority Incremental Budget System, which represents an economical compromise between Zero Based Budgeting and the Incremental Budgeting approach. For the actual preparation of the budget a budget committee is usually formed, comprising a representative from all departments, chaired almost inevitably by the chief executive.

Uses of Budgets and Budgetary Control

· Helps in planning and controlling of the organization's various departments and activities.

· Helps in using resources economically

· Helps in evaluating performance as the actual performance can be compared with the standards as in the budgets

· It provides a challenge to employees and thereby motivates them to meet the standards set.

· It makes the implementation of various strategies very smooth as every task is clearly decided in advance.

Features of a Good Control System

1. Appropriate : a control system should be appropriate to suit the requirements of the organisations depending on the scale of operations, size of the organisation, activity etc.

2. Economical: the costs of setting up a control system should not exceed the benefits derived from it.

3. Simple: the system should be simple enough to be understood by managers and workers alike. The set standards and the performance reports should be straight forward.

4. Objective: there should be very little scope for personal bias or partiality in the control system.

5. Flexible: it should be flexible enough to be changed and adjusted according to the changing requirements of the organisation.

6. Concentration on exceptions: the control system should focus on deviations that require action, any negligible differences should not be concentrated upon by the management as they can utilize their precious time on other serious and important matters.

Example: At Bell Atlantic senior level executives are appointed to specifically monitor corporate performance on the top 20 to 30 priorities. In this way, objectives are revisited, results analyzed, new conditions taken into account, and plans and activities adjusted to maximize performance. Such an independent review helps to ensure that the control process operates even at the highest levels of the organisation.

Test Your Knowledge

& Controlling is the process of ensuring that the actual activities conform to the planned activities (True or False)

& The first step in the control process is establishing ______________.

& A good control system helps deal with changes in the external environment (True or False)

& When the deviations are too high or low the _____________ may have to be re-set.

& Controlling may be carried out __________, ___________ and _______ the work process.

& Two techniques of managerial control are __________ and _____________.

& A _______ is a formal quantitative statement of resource allocations for planned activities during a period of time.

& A good control system should be simple enough to be understood by all. (True or False)

& A control system is said to be ____________ when it suits the requirements of the organisation.

& A good control does not allow any flexibility (True or False)

& Controlling helps evaluate the effectiveness of various other management functions (True or False)